How to Read Your Experian Credit Report (Simple Guide)

When you open your Experian credit report for the first time, it may feel slightly more detailed than a CIBIL report. There are more tables, more indicators, and more fields. That often makes people think Experian reports are difficult to understand.

They are not.

In reality, an Experian credit report follows the same basic structure as CIBIL. It just goes one level deeper by showing more behavioural and account-level details that lenders like to see. Once you know what to focus on, reading it becomes straightforward and actually very informative.

This guide explains each section of an Experian credit report in plain language, the way banks read it, without technical jargon or unnecessary complexity.

If you haven’t downloaded your report yet, you can start here: How to Download Your Free Experian Credit Report

For links to free reports from all Indian credit bureaus, you can also visit: Credit Reports

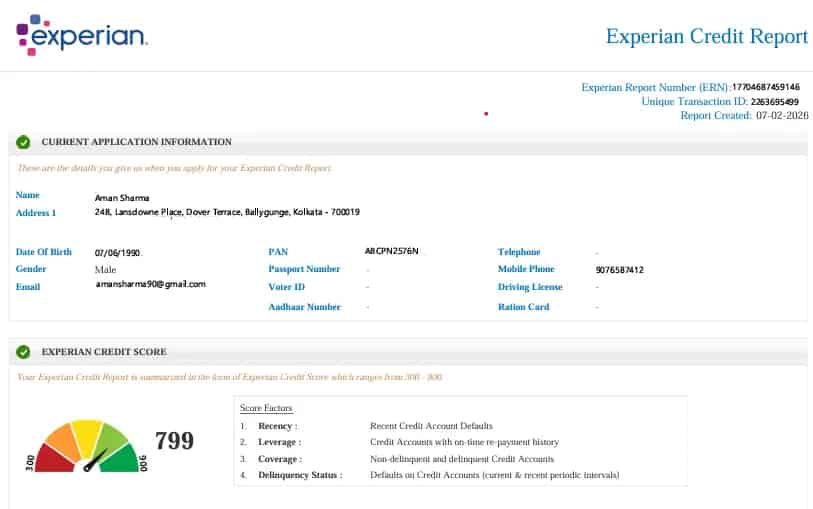

Report Header — Reference Information

At the top of your Experian credit report, you will see details like the Experian Report Number (ERN), a Unique Transaction ID, and the report creation date.

These details are purely administrative. They help Experian and lenders identify this specific report. They do not affect your credit score or loan eligibility in any way.

You only need these numbers if you ever contact Experian support or raise a dispute. For regular reading, you can move past this section.

Current Application Information — Your Identity Record

This section shows how your identity appears in the Experian database. It includes your name, date of birth, gender, PAN, contact details, and address information. You may also see references to other IDs such as Aadhaar, Voter ID, or Driving Licence if lenders have reported them.

This section does not impact your score, but it is critical for verification. Banks rely on it to confirm that the credit history belongs to the right person.

If you notice spelling mistakes, outdated addresses, or incorrect personal details, they should be corrected. Even though they don’t lower your score, such errors can create confusion during loan processing or KYC checks.

Experian Credit Score — The Summary Number

Your Experian credit score is a three-digit number between 300 and 900. Higher scores indicate lower risk.

For example, a score around 780–800 generally reflects strong repayment behaviour and responsible credit use.

That said, the score is only a summary. Banks do not approve loans based on the score alone. They always look at the underlying report to understand why the score looks the way it does.

Score Factors — Why Experian Feels More Detailed

Experian explains the score using a few internal factors. This is one reason the report feels more detailed than CIBIL.

These factors usually relate to:

- How recently you missed or delayed payments

- How much credit you are using compared to limits

- The mix of healthy and problematic accounts

- Any current or recent defaults

You don’t need to memorise these terms. The idea is simple: Experian is showing lenders whether your credit behaviour is stable, stretched, or risky.

Report Summary — The Quick Lender Overview

Before diving into individual loans, lenders look at the report summary. This section gives a high-level snapshot of your credit profile.

It usually covers:

- Total number of credit accounts

- Active versus closed accounts

- Total outstanding balance

- Secured and unsecured exposure

- Number of recent credit enquiries

Banks use this section to quickly judge overall credit health. Too many active accounts, high unsecured exposure, or frequent recent enquiries can raise caution, even before deeper checks.

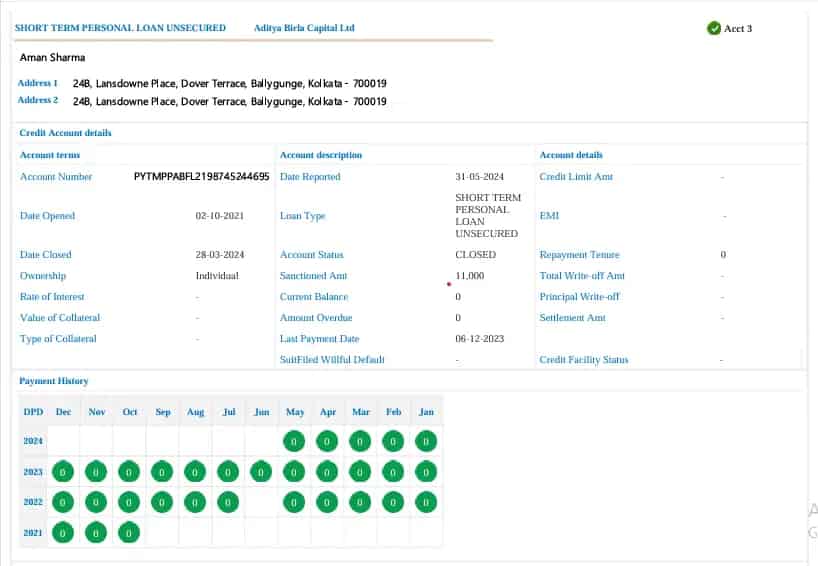

Credit Account Summary — Your Loan History

This section lists all loans and credit accounts reported to Experian, both active and closed.

Each entry shows the lender name, account type, ownership, key dates, sanctioned amount, current balance, overdue amount, and account status.

Banks scan this section to identify patterns:

- Are loans being closed properly?

- Are balances under control?

- Is there any account that stands out as risky?

Closed accounts with zero balance are a positive sign. Accounts showing overdue amounts or unusual statuses attract attention.

Credit Account Information Details — One Account at a Time

When banks want more clarity, they look at the detailed view of each account.

Here, you’ll see information such as:

- Date opened and closed

- Repayment tenure

- Last payment date

- Interest rate (if reported)

- Collateral details for secured loans

- Write-off or settlement amounts

This is where Experian provides more depth than CIBIL. It may look dense, but it helps lenders verify timelines and consistency.

Credit Facility Status — When You Should Pay Attention

In most healthy reports, the Credit Facility Status field is blank or marked with a dash. That usually means there is no adverse classification.

However, if this field shows terms like:

- Settled

- Written-off

- Post (WO) Settled

- Suit Filed

…it indicates that the loan did not end normally.

For unsecured loans especially, these statuses are serious red flags and can impact approvals for years, even if the loan was closed long ago.

Credit Enquiries — Signals of Borrowing Behaviour

This section lists all credit enquiries made by lenders, along with the date and purpose.

Occasional enquiries are normal. Multiple enquiries in a short span can suggest credit hunger or financial stress, even if no loan was finally taken.

Is Experian Harder Than CIBIL?

Not really.

If you understand a CIBIL report, Experian will feel familiar. The core sections are the same — personal details, credit accounts, payment history, and enquiries. Experian simply shows more internal indicators and account-level detail.

Once you know what matters, it becomes easier to read, not harder.

Lenders prefer borrowers who apply selectively and avoid unnecessary enquiries.

Final Thoughts — Read It Once, Use It Confidently

Your Experian credit report is not meant to intimidate you. It is a detailed record of how you have handled credit over time.

Focus on:

- Accuracy of personal details

- Clean account closures

- Consistent on-time payments

- Absence of serious status flags

Once you understand this report, you stop guessing why banks respond the way they do. You gain clarity and control — and that’s far more valuable than any single score.

0 Comments

No comments yet. Be the first to share your thoughts!